Securities and Exchange Commission of Sri Lanka (SEC) settlement with Musthaq Mohamed Fuad raises fresh questions over transparency, selective disclosure and regulatory credibility

Be that as it may, Sri Lanka’s financial regulatory architecture once again finds itself under uncomfortable scrutiny — not merely because of who was charged, but because of who allegedly was not publicly named.

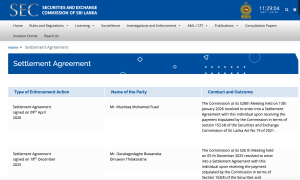

In April 2026, the Securities and Exchange Commission of Sri Lanka entered into a settlement arrangement with market participant Musthaq Mohamed Fuad under provisions available within the SEC Act, allowing the matter to conclude upon payment reportedly amounting to Rs. 5 million, thereby avoiding criminal prosecution.

Such settlements are not unlawful. In fact, many modern regulatory systems permit negotiated outcomes where admissions, penalties, compliance undertakings or financial settlements are deemed preferable to prolonged litigation.

But in Sri Lanka, context is everything.

Because the debate now is no longer merely about Fuad.

It is about opacity.

Market sources and individuals familiar with the matter allege that another individual had also faced regulatory action or was similarly implicated, yet that name — if true — has not entered the public domain. NEWSLINE at the time of publication could not independently verify the identity of the alleged second individual nor whether any formal settlement exists in relation to such a person.

That uncertainty has now collided with another deeply troubling development.

Chinthaka Mendis — the officer understood to have signed off on the charge sheet connected to the matter — has reportedly been interdicted amid allegations that he failed to disclose that a relative served as Chief Executive Officer of the Colombo Stock Exchange.

If accurate, the implications are severe.

Not necessarily because familial relationships exist — Sri Lanka’s professional ecosystem is notoriously small — but because regulatory legitimacy depends almost entirely on disclosure, procedural integrity and the avoidance of perceived conflicts of interest.

And perception, in markets, is often as dangerous as fact.

The concern now circulating among brokers, investors and governance observers is brutally simple:

Was there equal treatment?

Were all parties similarly exposed publicly?

Was there selective transparency?

And perhaps most importantly — who knew what, and when?

The SEC Act gives wide latitude for settlements. Regulators globally use such mechanisms to save time, reduce court burdens and secure compliance outcomes. But those same settlements demand extraordinary transparency if public confidence is to be preserved.

Otherwise, settlements begin to look less like regulation and more like negotiated discretion.

The interdiction of an officer tied to the process only deepens the optics crisis.

At the heart of this developing story lies a larger institutional problem that Sri Lanka repeatedly struggles with: governance systems that appear technically compliant, yet publicly distrusted.

That distinction matters.

Because markets do not operate merely on law.

They operate on confidence.

And confidence, once punctured, is expensive to restore.

The SEC, if it wishes to put speculation to rest, may eventually have to answer several uncomfortable questions publicly:

* Were there additional parties involved?

* Were all disclosures made appropriately?

* Were conflict protocols followed?

* And why has the matter generated so much uncertainty inside Colombo’s tightly wound financial ecosystem?

Until then, the story may remain less about a Rs. 5 million settlement — and more about whether Sri Lanka’s market watchdog itself can avoid becoming part of the controversy it was meant to regulate.

**NEWSLINE – The Daily By Faraz Shauketaly ** WhatsApp: +94 77 230 0305

*Questioning the Answers*