The financial implications of the alleged irregularities at National Development Bank PLC (NDB) extend far beyond the institution itself. While the immediate focus has been on the estimated loss of approximately Rs. 13.2 billion to the bank, a deeper economic analysis reveals a significant secondary impact a substantial loss of government revenue that would otherwise have been collected through taxation.

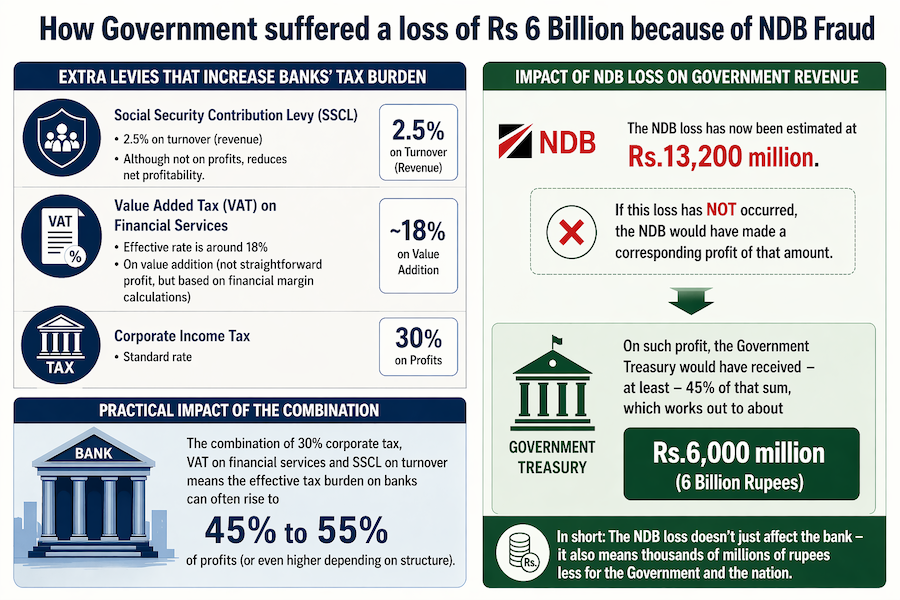

In Sri Lanka, banks operate under one of the heaviest tax regimes in the corporate sector. The base Corporate Income Tax (CIT) rate applicable to banks stands at 30% on taxable profits. However, this is only part of the story. Banks are also subject to additional levies that materially increase their overall tax burden. One such levy is the Social Security Contribution Levy (SSCL), currently imposed at 2.5% on turnover. Although it is not directly calculated on profits, it reduces the bank’s net earnings and, consequently, its retained profitability.

Further, banks are liable for Value Added Tax (VAT) on financial services. Unlike standard VAT, this is calculated on value addition essentially the financial margin making it more complex but nonetheless substantial. The effective rate of VAT on financial services is estimated to be around 18%, adding another significant layer to the tax burden.

When these components are combined 30% CIT, SSCL on turnover, and VAT on financial services the effective tax incidence on banks typically ranges between 45% and 55% of profits, and in some cases, even higher depending on operational structure and financial composition.

Against this backdrop, the estimated Rs. 13.2 billion loss at NDB takes on a broader fiscal dimension. Had this loss not occurred, it is reasonable to assume that the bank could have reported an equivalent level of profit. Applying a conservative effective tax rate of 45%, the Government of Sri Lanka would have potentially collected approximately Rs. 6 billion in tax revenue from this profit.

This figure represents a direct opportunity cost to the Treasury revenue that could have been utilized for public expenditure, debt servicing, or social welfare initiatives. In a macroeconomic environment where fiscal space remains constrained, such losses are not merely corporate setbacks but translate into tangible setbacks for the national economy.

Therefore, the issue is not confined to institutional governance or financial mismanagement alone. It raises broader questions about regulatory oversight, accountability, and the systemic consequences of failures within major financial institutions. The NDB case, in this context, serves as a reminder that banking sector lapses can have far-reaching implications ultimately borne by the public through lost state revenue and weakened economic resilience.

Banks in Sri Lanka pay Corporate Income Tax (CIT) at 30% on taxable profits (standard corporate rate).

In addition, Banks also face extra levies, which raise their effective tax burden well above 30%. These are:

- Social Security Contribution Levy (SSCL) which is 2.5% on turnover (revenue), and although not on profits, reduces net profitability.

- Value Added Tax (VAT) on Financial Services where the Effective rate is around 18% on value addition (not straightforward profit, but based on financial margin calculations).

The practical Impact of the combination of 30% corporate tax, VAT on financial services and SSCL on turnover is that the effective tax burden on banks can often rise to about 45% to 55% of profits (or even higher depending on structure).

The NDB loss has now been estimated at around Rs.13,200 million. If this loss has NOT occurred, the NDB would have made a corresponding profit of that amount. On such profit, the Government Treasury would have received – at least – 45% of that sum, which works out to about Rs.6,000 million.